Latest Update on the 1st Export Obligation Period under EPCG

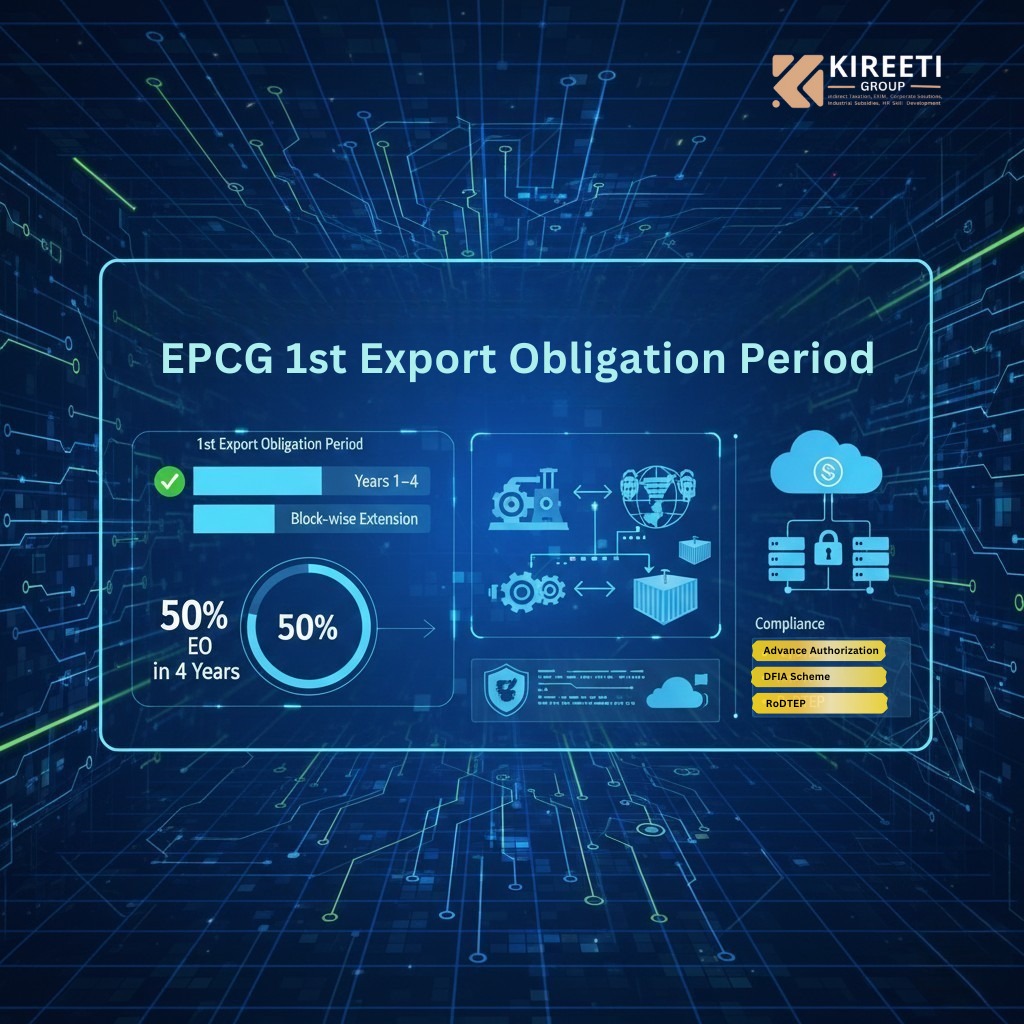

Under the Export Promotion Capital Goods (EPCG) scheme, the 1st Export Obligation Period (1st EOP) continues to be a key compliance benchmark for exporters. The fundamental requirement remains unchanged under the current policy framework: exporters must complete at least 50% of the specific export obligation within the first 4 years from the date of issue of the EPCG authorisation.

1st EOP – The core requirement remains intact

The EPCG scheme prescribes a specific export obligation (EO) equal to six times the customs duty saved on the imported capital goods, to be fulfilled within a total period of 6 years from the authorisation date. For monitoring and compliance purposes, this 6-year period is divided into two blocks:

- 1st Export Obligation Period (1st block): Years 1 to 4

Exporters are required to achieve a minimum of 50% of the total specific EO during this period. - 2nd block: Years 5 to 6

The balance export obligation—generally the remaining 50%—must be completed in this block, subject to any extension of the EO period granted by DGFT.

Recent policy and procedural changes have not altered this 50% within 4 years benchmark, which continues to be the primary test for compliance in the 1st EOP.

What has evolved around 1st EOP compliance

Although the quantitative requirement for the 1st EOP remains the same, DGFT has taken steps to make compliance and regularisation more practical where exporters are unable to meet the target within the first block. Key developments include:

- Continued provision for block-wise extension of the 1st EOP in cases where 50% EO is not achieved, subject to submission of a proper application to the Regional Authority (RA) and payment of applicable fees within prescribed timelines.

- Rationalisation and clarity in the fee structure, under which the composition fee is generally 2% of the proportionate duty-saved amount corresponding to the unfulfilled EO for that block, along with fixed government fees based on the duty-saved slab and the timing of the application.

These refinements are part of DGFT’s broader effort to soften the compliance impact for genuine exporters facing delays due to market conditions, project timelines, or operational constraints.

Practical relief for the shortfall in the 1st EOP

Exporters who are unable to meet the 50% EO requirement in the 1st EOP now have a clearer and more structured route to regularise the shortfall, rather than facing immediate duty recovery. In practical terms:

- Exporters may apply for a block-wise extension, allowing the unfulfilled portion of the 1st-block EO to be carried forward and merged with the remaining EO to be completed in the subsequent period, within the overall EO limit (typically extendable up to 8 years, subject to approval).

- DGFT has, through various circulars, also provided for condonation of delay in filing block-wise extension requests, subject to payment of additional fees, offering relief in cases where deadlines were missed earlier.

It is important to note that such relief is not automatic. Exporters must file complete applications, disclose EO details accurately, and pay the applicable composition and government fees.

What exporters should prioritise going forward

Since the substance of the 1st EOP requirement remains unchanged but the regularisation framework has become more facilitative, exporters should recalibrate their compliance approach around the 4-year milestone. Key actions include:

- Treat the 4-year / 50% EO requirement as a firm internal target and monitor progress through an updated EO tracking statement covering duty saved, EO fixed, and EO fulfilled.

- If a shortfall is anticipated, plan early for block-wise extension, including budgeting for the 2% composition fee on the unfulfilled EO portion and ensuring timely submission to the RA.

- Closely follow DGFT notifications, circulars, and public notices on condonation and EO-period extensions, as these may offer time-bound opportunities to regularise older or borderline cases.